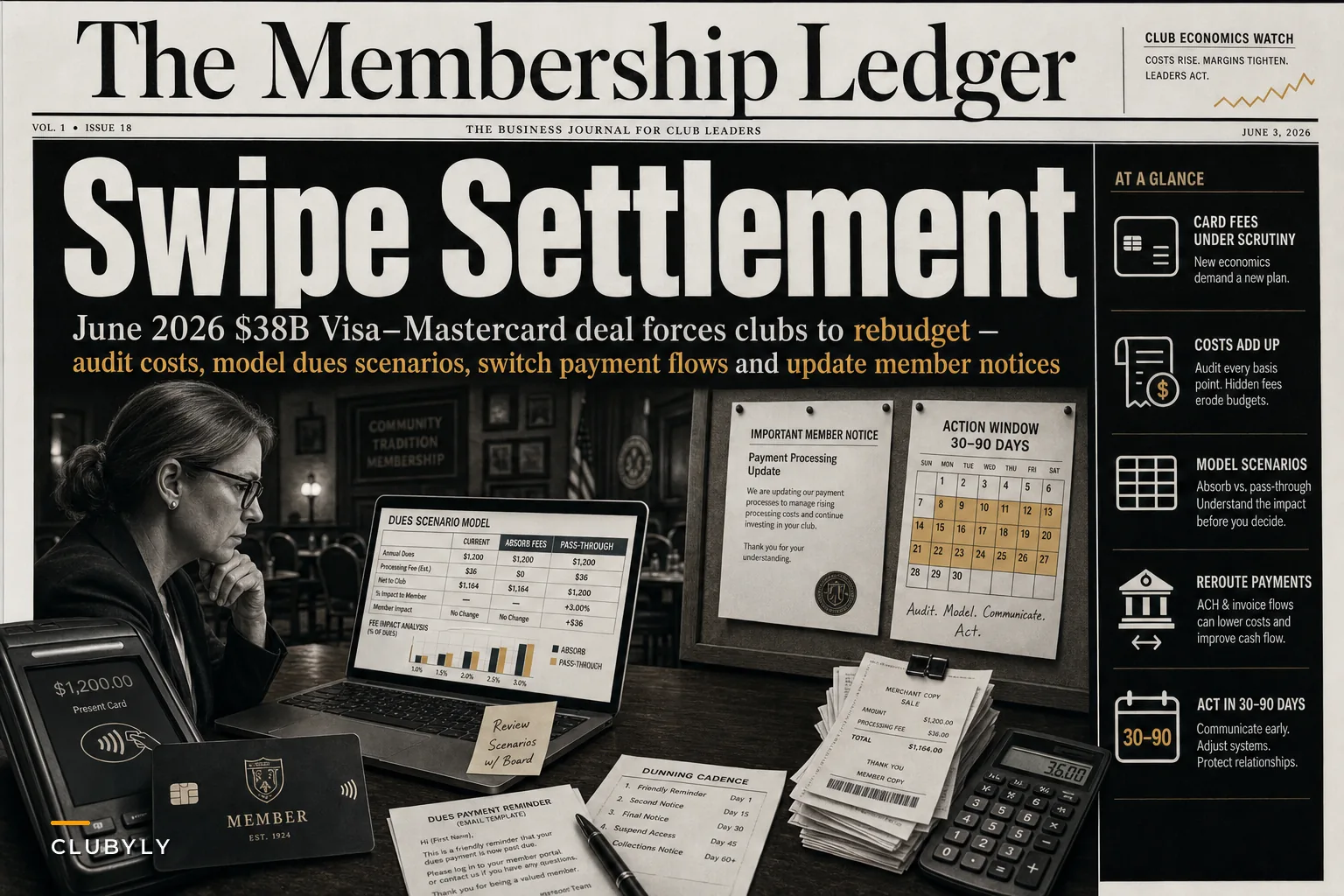

A federal judge approved a massive $38 billion settlement between Visa, Mastercard and merchants on June 9th. For clubs collecting monthly dues, event fees, and donation payments, this isn't just another headline—it's a real operational shift that hits your budget directly.

Most treasurers treat card processing fees like a fixed cost. Budget 2.5% or 3%, move on, repeat next year. But processing costs fluctuate based on card type, transaction size, and now potentially new surcharging rules that could let you pass fees to members for the first time.

The settlement opens doors for clubs to rethink payment economics entirely—not just tweaking a processor contract, but reconsidering how you collect dues, which payment methods you actually push members toward, and whether that convenience fee you've been quietly absorbing still makes any sense.

Card processing fees hide in every transaction—but clubs feel them differently

Running a youth soccer league with 400 families paying $85 monthly? At 2.9% + 30 cents per transaction, you're looking at roughly $1,200 in processing costs every month. Nearly $15k annually that could fund an extra scholarship or field rental.

The pain multiplies with small transactions. A $12 workshop fee or $8 guest pass can burn close to 6% once the fixed per-transaction cost gets factored in. A rowing club found their $15 locker rentals were costing $0.73 each to process—almost 5% gone before accounting for anything else.

What makes clubs particularly vulnerable is their transaction patterns. Recurring monthly dues create predictable but relentless fee accumulation. Event registrations spike fees during busy seasons. Small-dollar transactions carry disproportionate costs. And failed payment retries can double or triple the number of processing attempts on a single member's account.

The settlement changes the conversation from "processing fees are just the cost of doing business" to "we actually have options here."

Your processor contract probably needs a second look (especially the fine print)

Most club treasurers inherit their payment setup. Someone picked Square or Stripe a few years back, configured auto-billing, and nobody looked at it again. Meanwhile, fees compound quietly.

Keep your membership organized and engaged.

Clubyly simplifies member management, event coordination, and payment collection—effortlessly.

- Unified member database

- Automated payment tracking

- Event scheduling & reminders

No credit card required

A sailing club processing $280k annually in dues and event fees had been on the same processor for four years at 2.9% + $0.30. Nobody realized they qualified for nonprofit interchange rates (which saves roughly 0.4–0.6%) or that their volume justified negotiating closer to 2.4%. That oversight cost them around $2,800 a year.

The settlement creates real leverage for renegotiation. Processors know merchants are shopping around right now. Clubs have secured volume discounts at $100k+ annual processing, nonprofit rates for 501c3 organizations, reduced rates for ACH and bank transfers, waived monthly fees, and lower rates for recurring versus one-time transactions.

But negotiation only works if you understand your actual processing patterns. Pull six months of statements and calculate what matters:

| Metric | Why It Matters |

|---|---|

| Average transaction size | Larger transactions dilute fixed fees |

| Monthly volume | Leverage for rate negotiation |

| Card type mix (debit vs credit) | Different interchange rates apply |

| Failed payment rate | Each retry costs money |

| Refund/chargeback frequency | Hidden costs that add up fast |

Ask processors for an interchange-level fee breakdown so you can spot nonprofit or debit-rate opportunities.

Most clubs find their effective all-in rate is 3.2–3.5%, noticeably higher than whatever advertised rate they signed up for.

The ACH alternative most clubs overlook (and why members resist)

Bank transfers cost clubs somewhere around $0.25–$0.50 per transaction versus $3+ for a typical credit card dues payment. On paper, shifting everyone to ACH saves thousands. In practice, members resist giving out bank account numbers.

A tennis club tried pushing ACH-only for membership renewals. Renewal rates dropped 18% that quarter. Members cited security concerns, setup friction, and losing out on credit card rewards. The club reversed the policy within two months.

The smarter approach is graduated incentives that actually make economic sense:

-

Credit card

Full price + 2.9% convenience fee (now potentially allowed under new rules)

-

ACH

2% discount off dues

-

Annual prepay via check

5% discount

This structure worked for a community pool with 850 members. About 35% switched to ACH or annual prepay within six months, saving roughly $7k annually in processing fees. The discounts cost around $4k, netting $3k in savings plus better cash flow from the annual prepayers.

Being straight with members about the reason lands better than bureaucratic policy language. "We can keep dues lower if we reduce processing costs" is a message people actually respond to.

Surcharging gets real: the delicate psychology of passing fees to members

The settlement potentially expands merchants' ability to surcharge credit card payments. Just because you can doesn't mean you should—at least not without a plan.

A golf club added a 3% credit card surcharge without any warning. The backlash was fast. Board meetings turned into complaint sessions. Several long-time members threatened to quit. The club reversed course after three months, but the reputational damage stuck around longer than the policy did.

A sailing club handled it differently, and the contrast is pretty instructive. They gave three months advance notice with a clear explanation of rising operational costs. They offered multiple no-fee payment alternatives—ACH, check, annual prepay. They grandfathered existing auto-pay members for six months. And they were direct about where the money went: straight to payment processing, not into club revenue.

-

Announce the change at least three months out

-

Lead with the "keeping dues down" message, not the policy language

-

Make alternative payment options easy to set up before the deadline

-

Grandfather existing auto-pay members where you can

-

Be specific about what the fee covers—"payment processing costs," not vague "operational expenses"

The framing matters more than most treasurers expect. Members interpret surcharges as nickel-and-diming unless you tie it directly to keeping dues increases minimal, offer real no-fee alternatives, show where the money actually goes, and give enough runway to make the switch.

When payment failures cascade into membership losses

Card processing fees aren't just about successful transactions—failed ones cost money too. Every declined payment triggers a retry, each carrying its own fee. And a weak dunning process turns a payment hiccup into a permanent member loss.

A cycling club had an 11% monthly payment failure rate, mostly from expired cards and insufficient funds. Each failure triggered three automatic retries over ten days. With 600 members paying $45 monthly, that translated to roughly 200 failed attempts per month—burning $500+ in fees on transactions that never went through.

Fixing your dunning process matters more now that processing economics are shifting. Every prevented failure saves the fee and reduces the risk of someone quietly churning out. This is exactly why building a solid dunning playbook to recover failed payments is worth the effort before problems compound.

-

Day -7

Email reminder that payment is upcoming

-

Day 0

Initial charge attempt

-

Day 3

Retry if failed, with SMS notification

-

Day 7

Second retry, treasurer CC'd on email

-

Day 10

Personal outreach from membership chair

-

Day 14

ACH/check payment option offered

-

Day 21

Suspension warning

-

Day 30

Membership suspended

One swim club reduced their payment failure rate from 12% to 4% using this structure, saving around $3k annually in failed transaction fees alone.

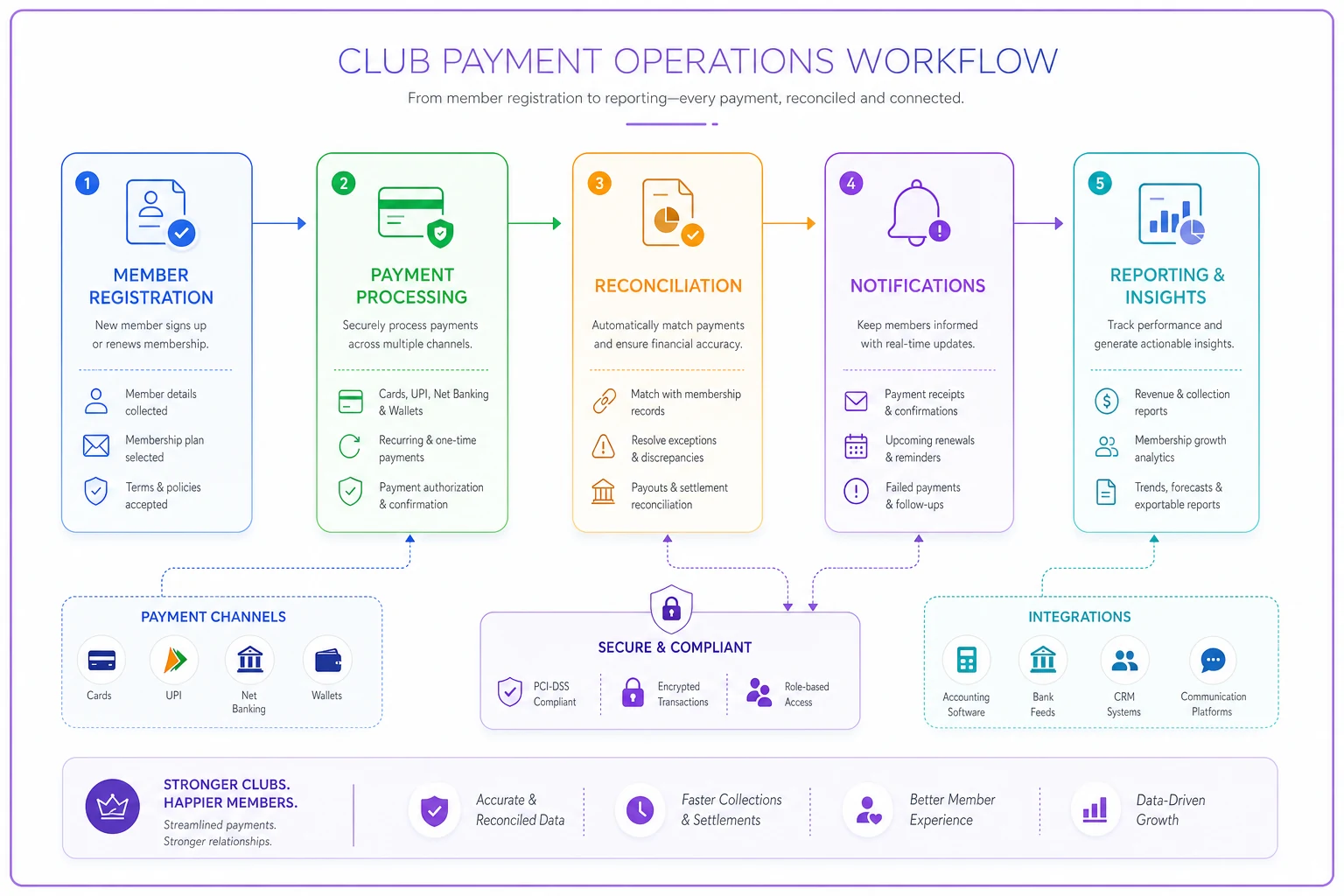

Building a payment operations workflow that scales with your club

Payment processing doesn't operate in isolation. It connects to membership tracking, event registration, financial reporting, and member communications. Most clubs end up cobbling together Stripe plus Google Sheets plus manual reconciliation—and the treasurer eats 10–15 hours of work every month stitching it all together.

A running club hosting four races annually with 200–300 participants per event ran their workflow like this:

-

Collect registrations via Google Forms

-

Process payments through Square

-

Manually match payments to registrations

-

Email confirmations one by one

-

Track no-shows and refunds in a spreadsheet

-

Reconcile everything for the monthly board report

Each race consumed 20–30 hours of volunteer treasurer time. One data entry error during their spring 5K left 15 runners showing up without confirmed registrations—entirely preventable race-day chaos.

Centralized operational platforms handle registration, payment, confirmations, and reporting in one place.

Visualize this workflow:

More importantly, when card processing fees change—which they might post-settlement—you update the rules once rather than hunting through multiple disconnected tools. That kind of setup also enables more sophisticated fee strategies without adding manual work: different rates for member versus non-member event registration, early-bird pricing that shifts automatically, group discounts that calculate correctly, payment plans for expensive programs, automatic tax calculation on merchandise.

Your 90-day action plan for the new payment landscape

The settlement won't flip everything overnight, but clubs that start now will be in a better position when processors start adjusting terms. A practical timeline:

Next 30 days: Audit current state

Pull your last six months of processing statements. Calculate your effective rate—total fees divided by total processed. Most clubs land somewhere between 3.2–3.5% all-in, higher than whatever advertised rate they're paying.

Document how dues get collected, how event fees work, and how donations come in. Each might need a different optimization approach.

Survey members about payment preferences. Ask directly whether they'd use ACH for a 2% discount or prepay annually for 5% off. The answers are often more useful than assumptions.

Days 30–60: Explore alternatives

Get quotes from at least three processors. Mention you're reviewing options in light of the settlement—it tends to sharpen the conversation. Include one processor that specializes in nonprofits if your club qualifies.

Research your state's surcharging laws. Analysis from Payments Dive shows rules vary significantly—some states still prohibit certain surcharges entirely.

Test ACH setup with your board or volunteer team before rolling it out to the full membership. Iron out the friction points first.

Days 60–90: Implement changes carefully

If you're adding surcharges, announce it at least three months ahead of implementation. Keep the messaging simple: "The 2.9% fee ensures your full $85 dues goes to club operations rather than payment processing."

Launch incentives for alternative payment methods starting with new members, so existing auto-pay setups don't get disrupted immediately.

Tighten your dunning process to reduce failed payment retries. Every prevented failure saves money under any fee structure.

The bottom line on payment economics

The Visa–Mastercard settlement is an inflection point, not a complete overhaul. Processing costs will stay significant for clubs, but there are more tools available now to manage them than there were a year ago.

Clubs that handle this well will treat payment operations as a strategic function rather than an administrative chore. They'll blend multiple payment methods, be direct with members about costs, and use operational platforms to cut down on the manual reconciliation work that quietly consumes treasurer hours every month.

Members don't know what interchange rates are and don't need to. They care about convenient payment options, transparent pricing, and knowing their dues are actually going toward club activities. Get the operational side right and you can deliver all three while trimming your processing costs at the same time.

Start with that processor contract sitting in your files. Run the numbers on your actual effective rate. Survey members on what they'd realistically switch to. Small steps now prevent thousand-dollar leaks later.

Ready to streamline your club operations?

Join 500+ clubs using Clubyly to save time, boost member engagement, and grow their communities.